Figma: The Collaborative Design Powerhouse

A category-defining design platform with rapid growth, sticky economics, and a rich IPO valuation testing investor conviction.

TL;DR

Figma is going public on July 31, 2025 with a ~$19B valuation (~25× 2024 revenue), positioning itself as the dominant cloud-native design platform.

The company boasts 53% revenue CAGR, 132% net dollar retention, and 88%+ gross margin, reflecting strong fundamentals and product-market fit.

Its freemium model, real-time collaboration, and cross-functional reach have disrupted incumbents like Adobe and Sketch.

Valuation scenarios project 6–24% annualized returns by 2030 depending on growth, multiple, and dilution assumptions.

While the business is exceptional, the stock is not obviously cheap — best risk/reward is below $30/share with a starter 0.5% position.

Introduction

Figma, a cloud-native, collaborative design platform, is preparing to go public on July 31, 2025, under the ticker “FIG” on the NYSE. As a category-defining software company that reimagined how designers, developers, and product teams collaborate, Figma represents a compelling opportunity at the intersection of product-led growth, SaaS monetization, and generative AI enablement. This investment thesis aims to evaluate Figma’s business, fundamentals, competitive positioning, and long-term growth prospects in the context of its upcoming IPO.

Founded in 2012 by Dylan Field and Evan Wallace, Figma was built with a bold vision: to make design accessible to everyone through a collaborative browser-based platform. After years of development in stealth, Figma launched publicly in 2015 with a groundbreaking real-time multiplayer canvas—ushering in a new era of synchronous, cross-functional design. Its freemium model, ease of access, and viral product-led growth strategy quickly gained traction, initially among individual designers and later with enterprise teams.

Today, Figma operates a robust subscription-based model with strong network effects and high retention. In 2024, the company generated $749 million in revenue, highlighting its rapid growth trajectory. As it enters the public markets with a proposed valuation of approximately $19 billion (~25x 2024 revenue), investors must weigh both the scalability of its business model and the execution risks ahead. Key areas to assess include Figma’s leadership in UI/UX design, its expansion into adjacent markets like whiteboarding and slides, the disruptive potential of AI, and intensifying competition from firms such as Canva and Miro.

Business Model

Figma operates on a freemium, subscription-based model built around its collaborative, cloud-native design platform, hosted on Amazon Web Services. It supports UI/UX design, graphic design, prototyping, and wireframing, enabling real-time collaboration across teams. Unlike traditional desktop tools, Figma fosters cross-functional synergy, streamlining workflows across product, design, and engineering.

Freemium Model

Figma’s free Starter plan offers unlimited files (up to 3 pages per file) and access for up to three editors, encouraging adoption by individuals, startups, and students. It serves as a core engine for product-led growth, with free usage often converting to paid plans. Educational adoption seeds long-term loyalty and future upgrades.

Paid Subscriptions

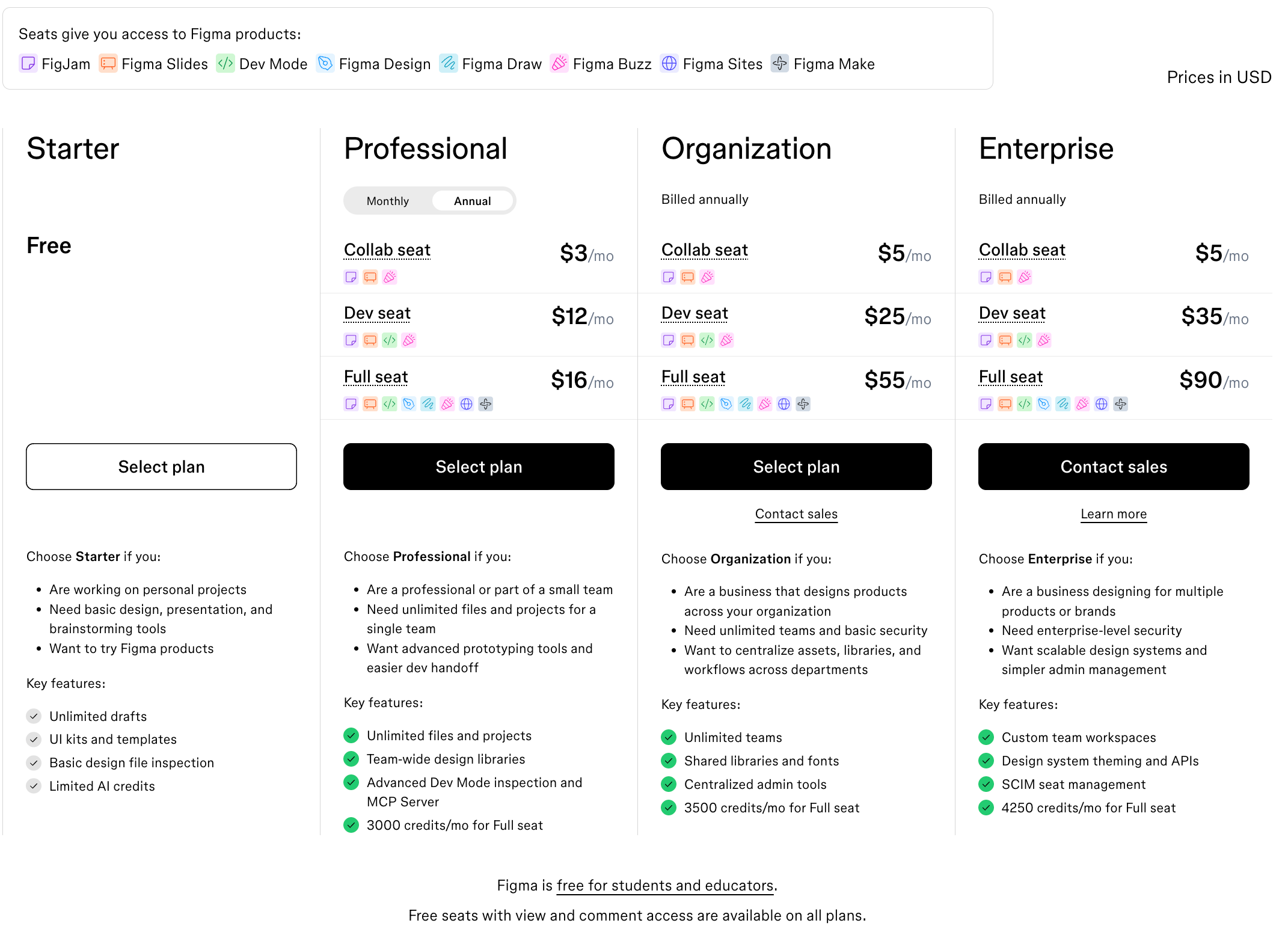

Figma’s revenue primarily comes from tiered subscription plans:

Professional Plan ($16/editor/month): Unlimited files, team libraries, and advanced prototyping for small teams.

Organization Plan (from $55/month): Enhanced security, shared fonts, and admin controls for enterprise-scale collaboration.

Enterprise Solutions: Custom offerings for large clients with deep integrations (e.g., Slack, GitHub, Jira) and premium support. Major customers include Microsoft, Airbnb, and SAP.

Additional Revenue Streams

FigJam: Launched in 2021 and monetized in 2022, this collaborative whiteboarding tool extends Figma to non-design roles, such as PMs and educators. A Forrester study commissioned by Figma cites a 328% ROI for companies using both Figma and FigJam.

Figma Community: Users can sell plugins and templates, with Figma taking a 15% commission—creating a flywheel of innovation and revenue.

Educational Partnerships: Discounted plans for schools build early familiarity, positioning Figma as the default for future professionals.

Growth Engine: PLG & Community-Led Strategy

Figma’s growth is powered by Product-Led Growth (PLG) and Community-Led Growth.

PLG: Figma’s intuitive UI and real-time features drive viral adoption. A single designer can bring in teams organically. As product managers and developers interact through comments or edits, organizations often upgrade. Deep integrations with Slack and GitHub help embed Figma into existing workflows.

Community-Led Growth: Through events like Config, product livestreams, forums, and plugin development, Figma nurtures a vibrant community that promotes, builds on, and advocates for the platform. This reduces internal support needs while scaling reach and loyalty.

Revenue Mechanics

Figma sells subscriptions on a per-seat basis, billed upfront, with revenue recognized over the contract term. Much of reported revenue stems from earlier bookings.

Customer Plans

Starter (Free) – Entry point for individuals.

Professional – Teams needing advanced design tools.

Organization – Multi-team setups with centralized controls (launched 2018).

Enterprise – High-scale customers (launched 2022).

Seat Types

Viewer (Free)

Collab – FigJam and Figma Slides

Content – Buzz, Sites CMS, FigJam, Slides (beta)

Dev – Dev Mode + all above

Full – All products (Make, Buzz, Draw, Sites, etc. in beta)

Pricing & Packaging (2025 Update)

In March 2025, Figma:

Made seat upgrades admin-controlled (vs. self-serve).

Raised Full seat pricing by 20–33% (😳) to improve transparency and controls.

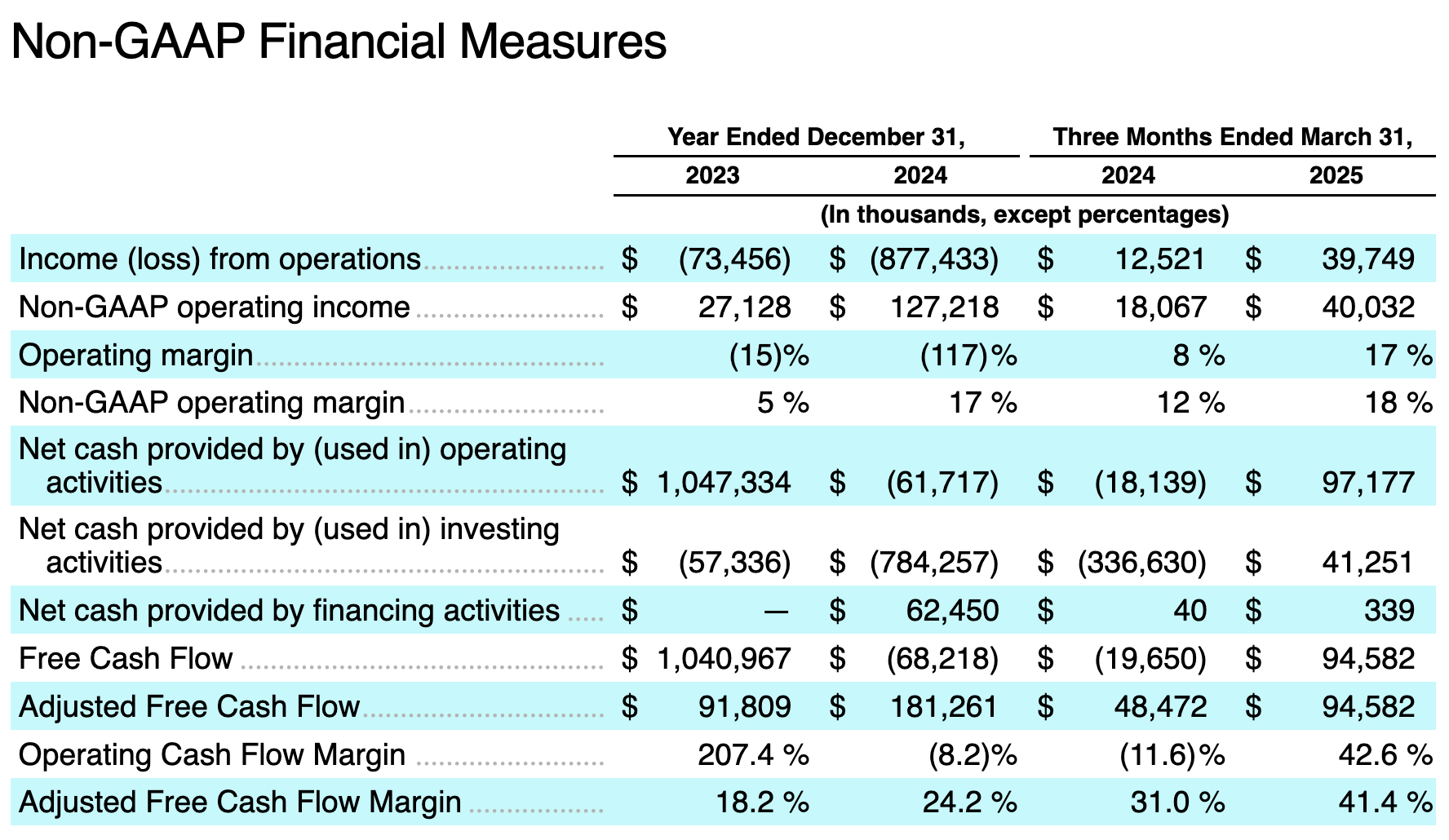

Financial Performance

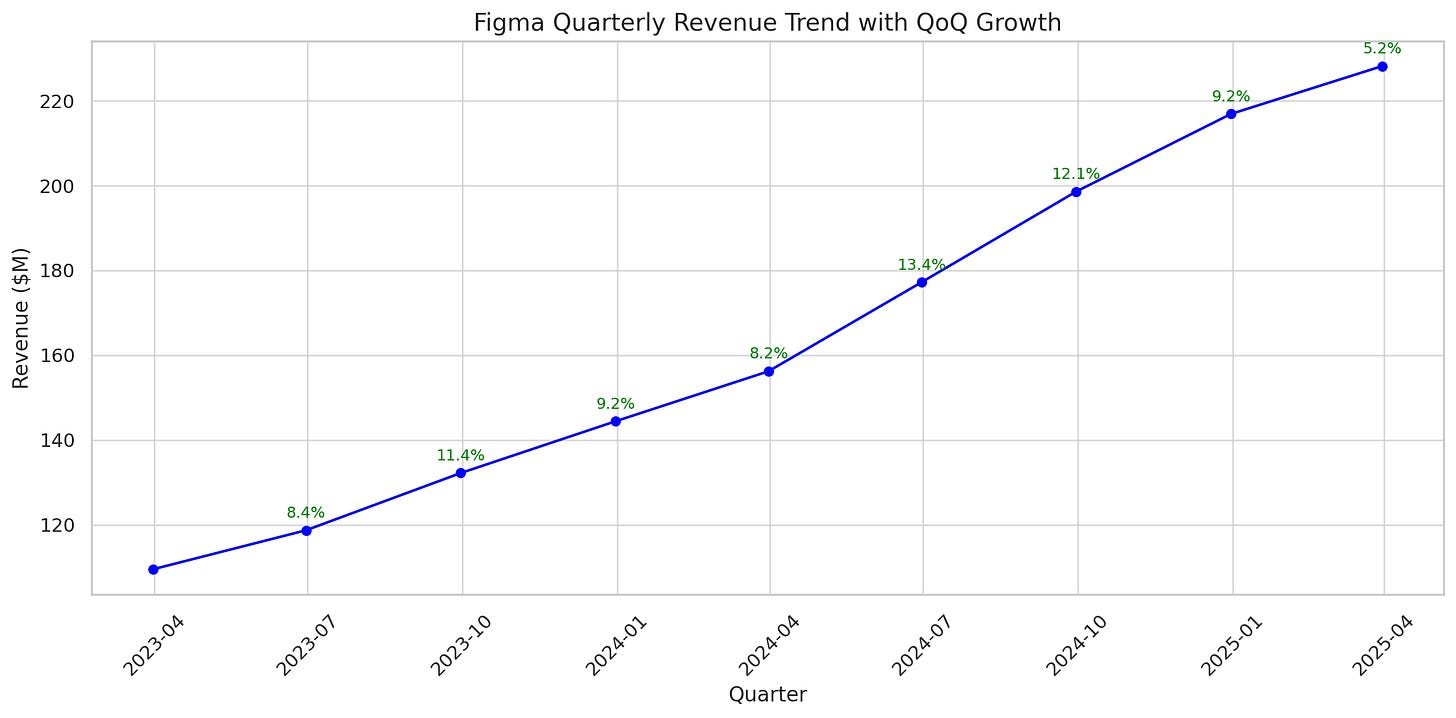

Figma's four-year compounded annual revenue growth rate as of December 31, 2024, was 53%.

Revenue: Figma has maintained impressive revenue growth rates.

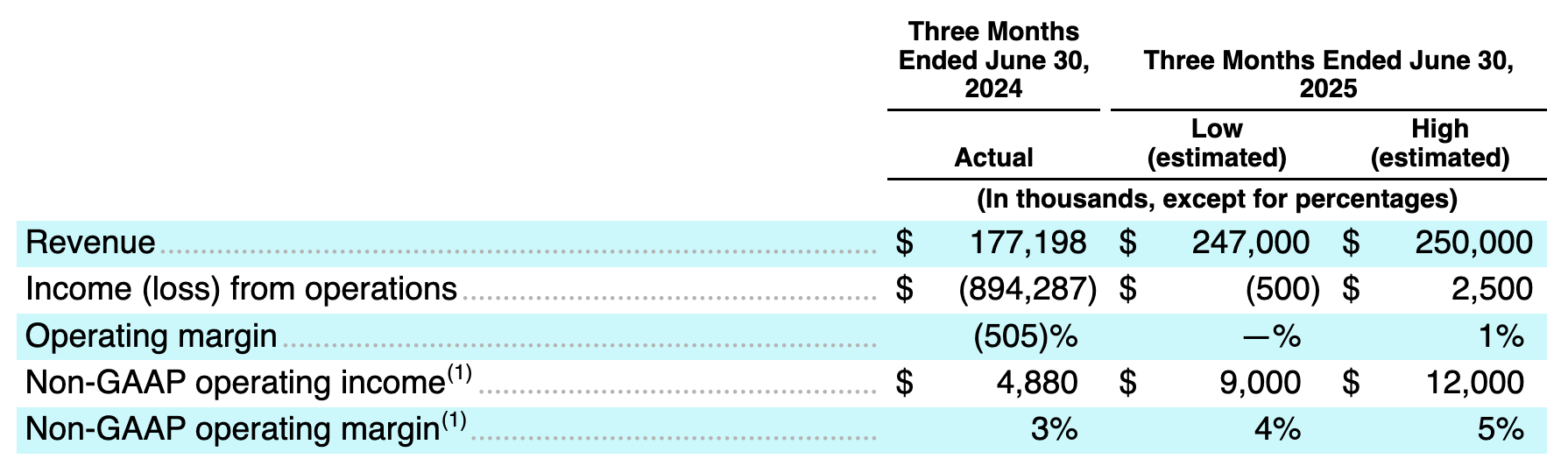

In Q1 2025, the company reported $228.2 million in revenue, representing a substantial 46% year-over-year growth.

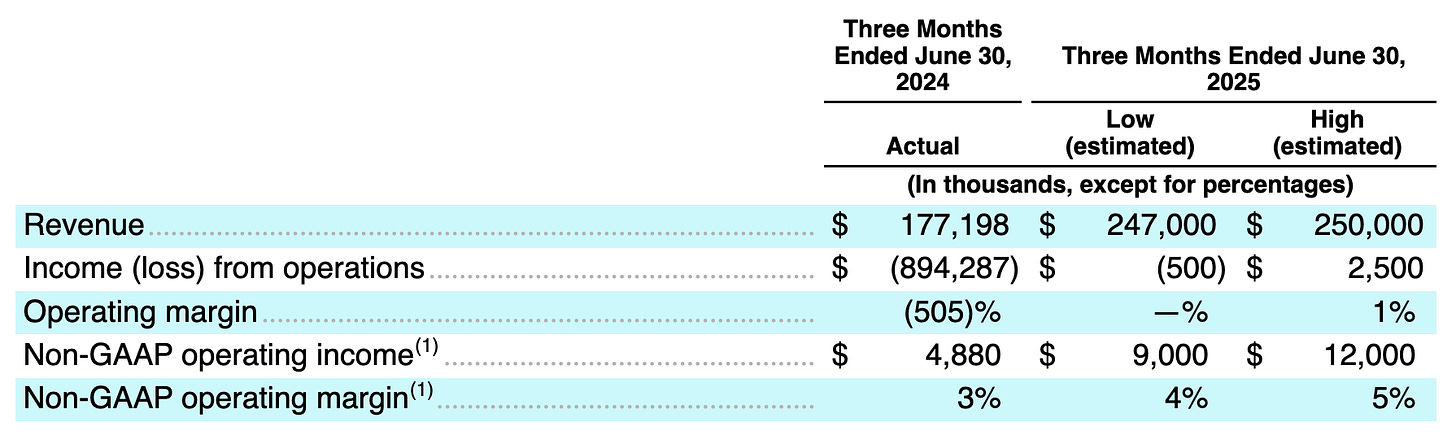

Preliminary results for Q2 2025 indicate continued momentum, with revenue projected to be between $247 million and $250 million, reflecting a healthy 39–41% year-over-year growth. While the growth rate has slightly decelerated as the company scales, it remains exceptionally strong for a business of its size.

Q2 2025 Profitability: Preliminary results for Q2 2025 indicate an operating margin of 3–5%. Compared to Q1 2025, this margin is modest, suggesting potential seasonality in operating expenses.

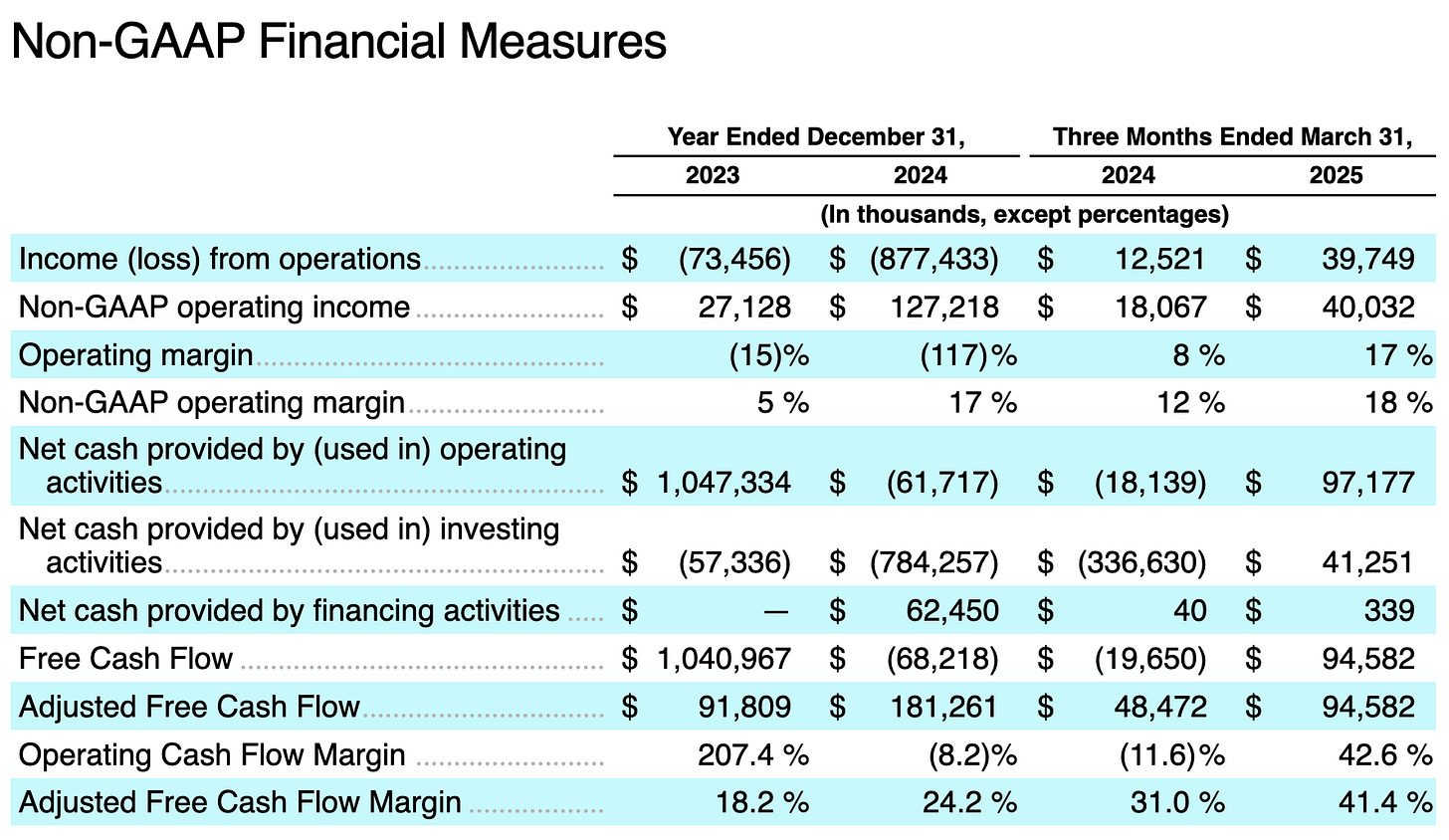

Q1 2025 Profitability: In the Q1 2025, Figma significantly improved its profitability, reporting a net income of $44.9 million—more than triple the $13.5 million reported in Q1 2024. Operating income reached $39.7 million, with an operating margin of 17%, while non-GAAP operating income came in at $40.0 million, yielding an 18% non-GAAP operating margin.

Customers: Figma's customer base continues to expand both in number and value.

As of March 31, 2025, Figma served a total of 450,000 customers.

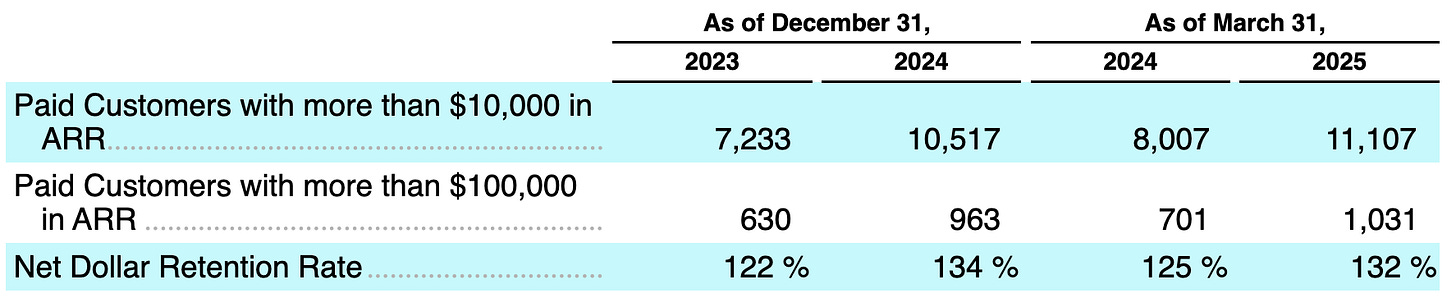

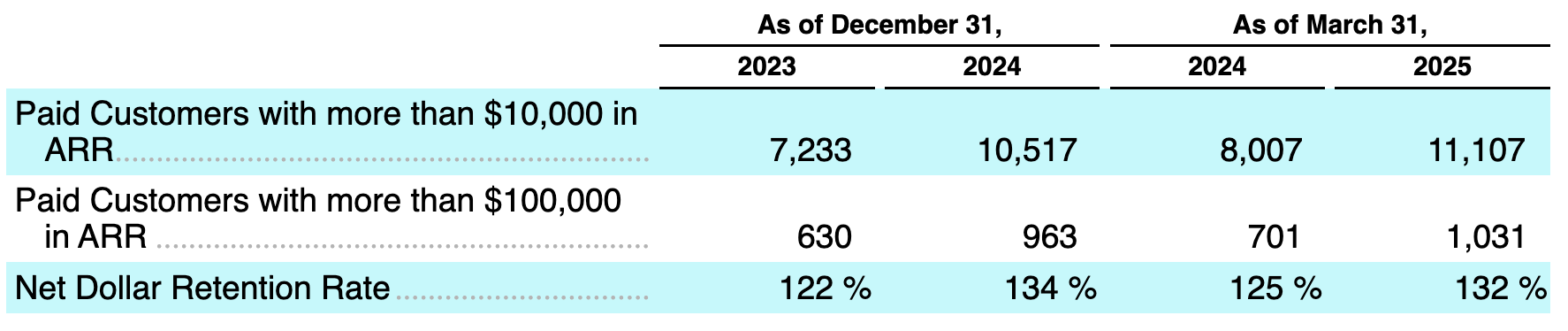

Crucially, 1,031 of these customers contributed at least $100,000 annually to revenue, marking a impressive 47% year-over-year growth in this high-value segment. This highlights Figma's success in penetrating and expanding within large enterprises, which are sticky and provide substantial recurring revenue.

The company also boasts 13 million monthly active users (MAUs), with a significant 85% located internationally, underscoring its global reach and broad appeal.

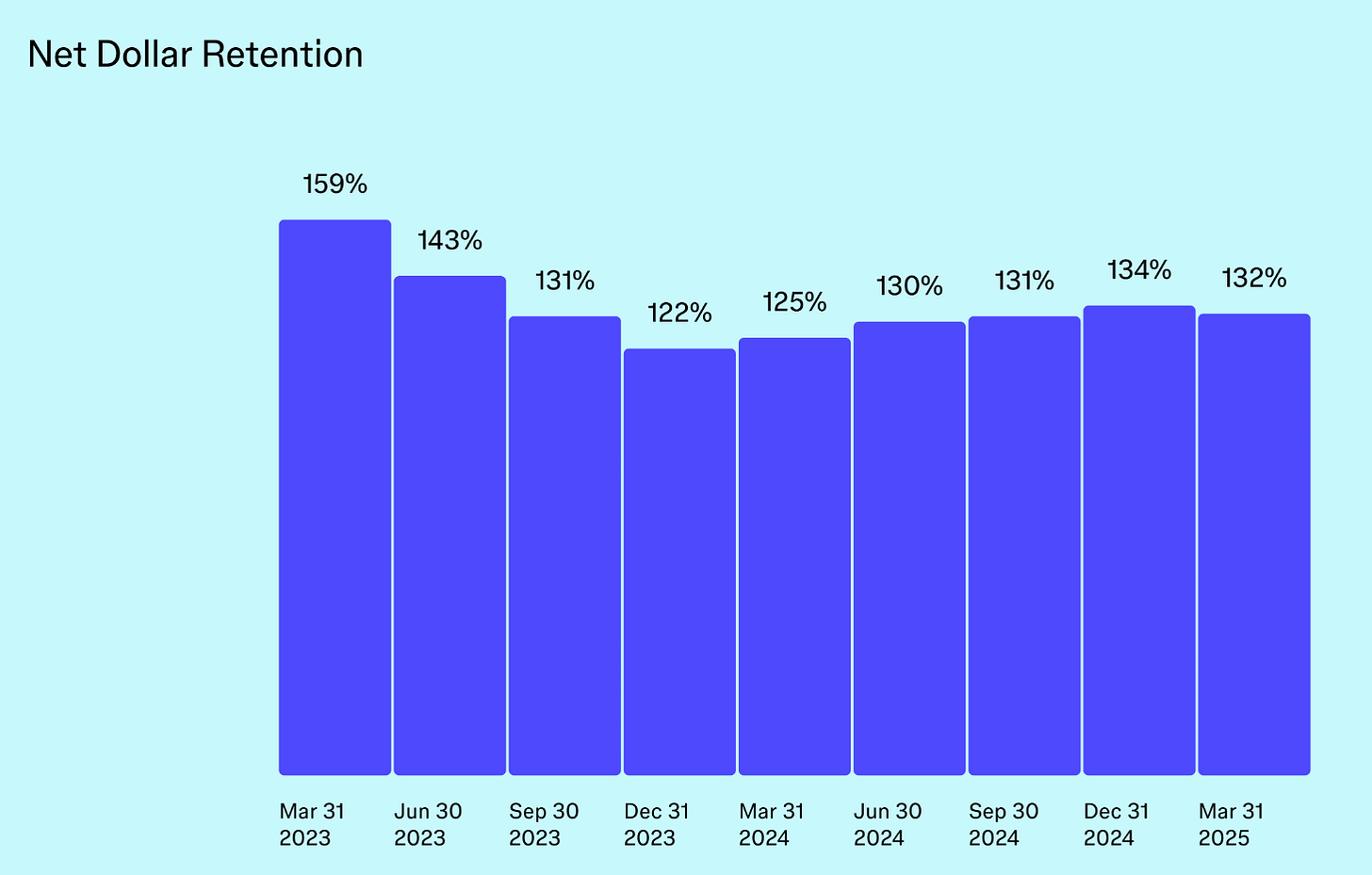

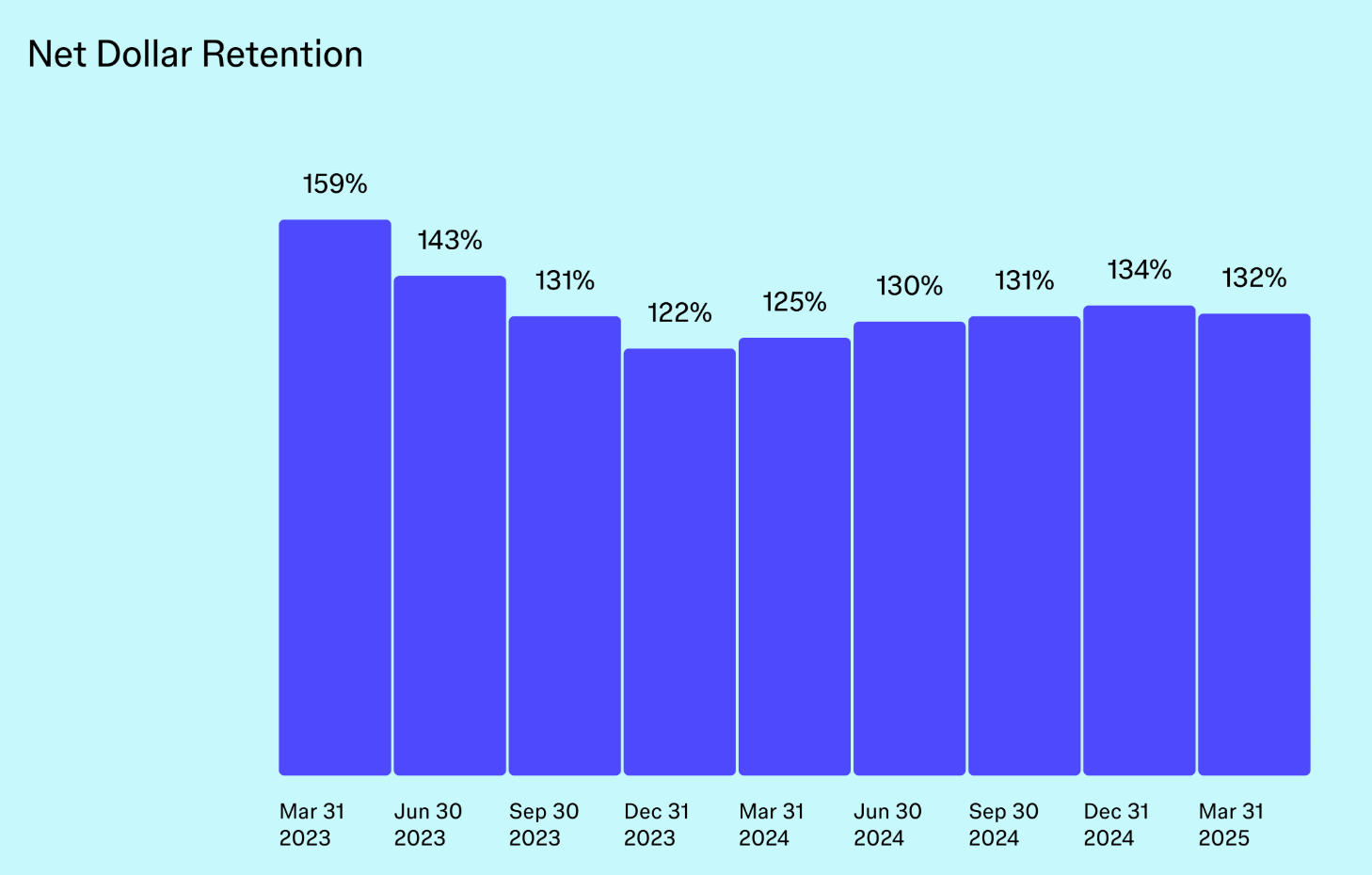

Net Dollar Retention Rate (NDRR): Figma defines this metric as the ability to retain and grow revenue within the existing customer base for Paid Customers with more than $10,000 in ARR. Figma's NDR of 132% is an exceptionally strong metric for a SaaS company. It means that existing customers with $10,000 ARR, on average, are spending 32% more this year than last year, either through upgrading to higher-priced plans, adding more users, or expanding their usage to complementary products like FigJam. This indicates robust customer satisfaction, successful "land and expand" strategies, and a valuable product that customers increasingly rely on

Gross Margin: With an 88.3% gross margin in Q1 2025, Figma demonstrates the highly favorable economics typical of successful SaaS businesses. This high margin indicates that the cost of delivering its service is low relative to the revenue it generates, providing ample room for reinvestment in R&D, sales, and marketing, or for increased profitability.

One-Time Revenue: In 2023, Figma received a $1 billion termination fee from Adobe following the abandonment of their proposed acquisition due to antitrust concerns. While a significant cash infusion that boosted Figma's overall financial position, it is important to note that this was a one-time event and does not contribute to the company's recurring revenue or ongoing operational performance. This fee, however, underscores Figma's strategic value and the competitive threat it posed to established players like Adobe.

Growth Strategy

Product Innovation: Figma drives growth through rapid product development, launching tools like FigJam, Dev Mode, and AI-powered features to expand its use across the design-to-code workflow. Nearly half of its workforce is dedicated to R&D, signaling deep commitment to innovation.

User Conversion: By offering free plans and educational access, Figma attracts users who often upgrade to paid tiers—70% of Organization and Enterprise customers previously used lower-tier plans.

Customer Expansion: Figma grows within existing accounts by launching complementary tools, reflected in a strong 132% net dollar retention rate and significant untapped revenue potential among Global 2000 clients.

Platform Extensibility: The company enhances value through a plugin ecosystem and Community sharing platform, making it easy for users to extend Figma’s functionality to fit their needs.

International Growth: While 85% of users are outside the U.S., only 53% of revenue is international—highlighting a major opportunity Figma pursues with multilingual support, currency localization, and global offices.

Strategic M&A: Figma accelerates innovation and ecosystem growth through acquisitions and investments, including over 10 deals and 18 venture investments by March 2025.

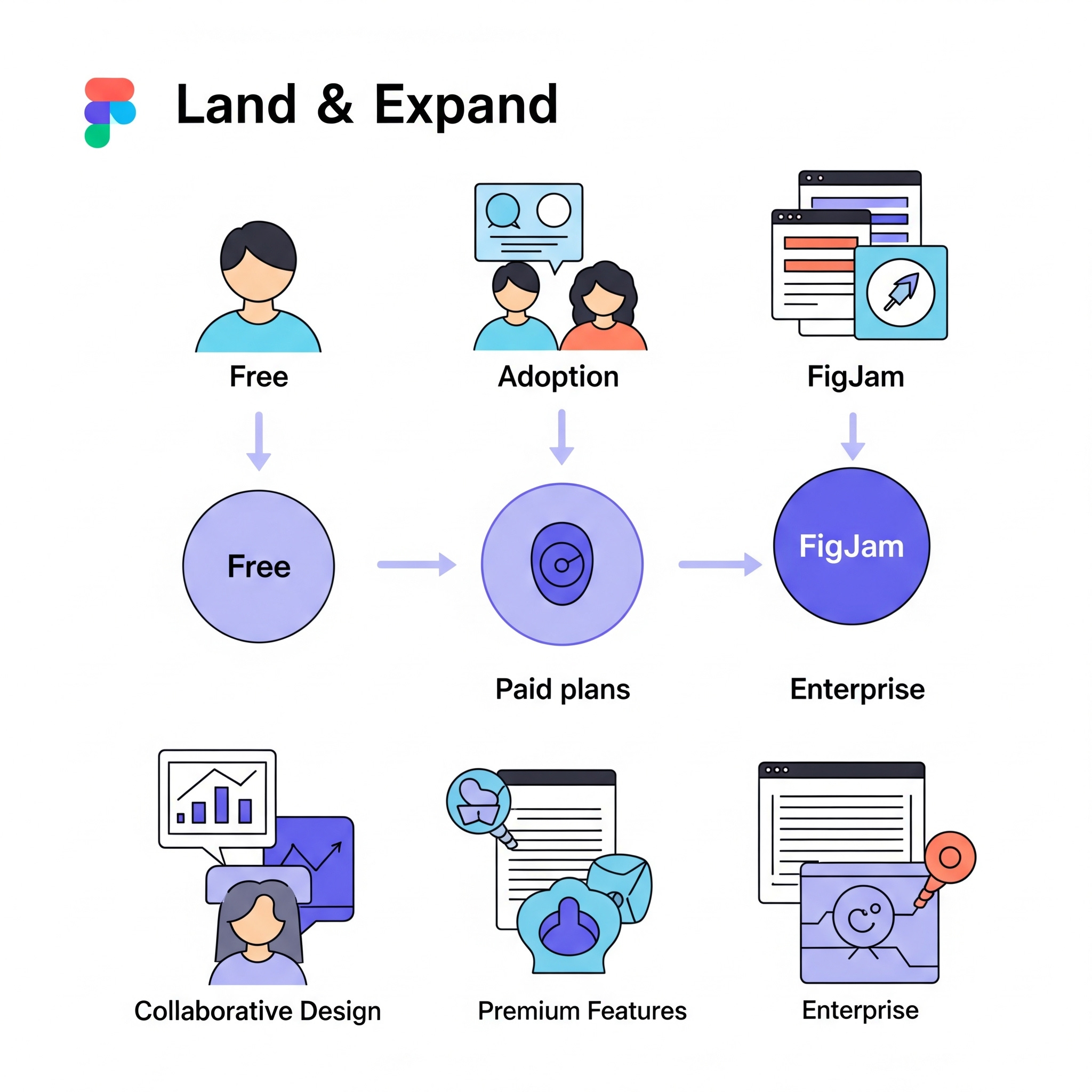

Illustrating Figma’s Land and Expand

This illustration visualizes Figma's "Land and Expand" business model. It begins with free initial adoption, where users try out the platform at no cost. As their needs grow, they upgrade to paid plans for more premium features. This expanded usage eventually leads to enterprise-level integration, where Figma becomes a core tool across the entire organization. This also shows the diversification into complementary products like FigJam, highlighting how Figma captures various collaborative design and workflow needs, ultimately driving increased revenue.

Understanding the Moat

Figma’s Counter-Positioning Strategy

Counter-positioning involves adopting a business model that established players can't easily mimic without threatening their core revenue or operations. Figma used this approach to challenge incumbents like Adobe and Sketch—not by iterating on existing tools, but by rethinking how design software is accessed, used, and monetized.

Cloud-Native Collaboration vs. Desktop-Centric Tools

While Adobe and Sketch relied on desktop-based apps with cumbersome file sharing and version control, Figma was built for the browser using WebGL. This enabled seamless real-time collaboration—akin to Google Docs—eliminating version conflicts and making team workflows more efficient. Incumbents, anchored in legacy architectures, couldn’t match this without overhauling their platforms, risking revenue disruption. Adobe XD’s partial cloud features never reached Figma’s fluidity.

Freemium Access vs. Expensive Subscriptions

Adobe and Sketch charged high fees with limited trials, targeting professionals. Figma flipped the script with a powerful free Starter plan for up to three editors, democratizing access for individuals, students, and small teams. This low-friction entry fueled adoption and retention, especially during periods of low employment or hobby usage—where Adobe’s paid-only model alienated users.

Cross-Functional vs. Designer-Centric Utility

Legacy tools served only designers, sidelining developers and product managers. Figma embedded itself across teams: Dev Mode enabled engineers to inspect files directly; FigJam appealed to PMs for brainstorming. This cross-functional reach created viral, internal adoption loops that incumbent design tools couldn’t replicate due to their narrow focus.

Community-Led Ecosystem vs. Closed Platforms

Figma built an open, transparent ecosystem through its Community platform and APIs, inviting users to share plugins and templates. In contrast, Adobe maintained tight control over Creative Cloud’s ecosystem. Figma’s open structure encouraged innovation, deepened user trust, and amplified loyalty, differentiating it from Adobe’s perceived opacity and rigidity.

Workflow-Centric Messaging vs. Feature-Driven Tools

Instead of marketing itself solely as a design tool, Figma positioned itself as a complete workflow solution. Messaging focused on team collaboration and faster product cycles—appealing to product leaders and decision-makers, while Sketch remained focused on design features alone.

Proof of Disruption

By 2021, Figma had claimed 77% of the product design market, overtaking Adobe XD and Sketch. Adobe’s $20 billion acquisition attempt in 2022, later blocked by regulators, confirmed Figma’s disruptive threat. The deal illustrated that Adobe couldn’t compete without cannibalizing its own core business.

Figma’s cloud-first, freemium, and cross-functional platform directly challenged incumbent models rooted in high-cost, designer-only, desktop software. This counter-positioning gave Figma a defensible edge, redefining the market and forcing legacy players into a reactive posture.

Figma’s Scale Economy

Figma benefits from a strong scale economy driven by its cloud-native SaaS model, high operating leverage, and viral freemium distribution. As a browser-based platform, Figma incurs minimal incremental costs to serve additional users, which allows gross margins to expand as revenue grows. Its freemium model acts as a self-service growth engine, enabling widespread adoption without proportional increases in sales or marketing spend. Users can explore the product for free and naturally convert to paid plans as their needs evolve—resulting in efficient customer acquisition and retention. This dynamic is evident in Figma’s improving profitability, with non-GAAP operating margins increasing from 3% in Q2 2024 to an estimated 4–5% in Q2 2025, despite ongoing investment in innovation and expansion.

Figma’s scale advantage is further amplified by cross-functional network effects and a shared product infrastructure. As more roles across design, engineering, and product teams adopt Figma, the platform becomes more embedded, increasing its value and stickiness. Switching costs rise, churn decreases, and net revenue retention improves—reaching 132% as of Q1 2025. Additionally, Figma leverages its core multiplayer canvas and real-time collaboration infrastructure across multiple products (Design, FigJam, Dev Mode, Slides, Sites, Make), spreading R&D costs across a growing revenue base. The Figma Community also contributes to scalability by allowing users to create and distribute plugins, templates, and widgets, enriching the ecosystem at minimal cost to Figma. These compounding advantages allow the company to scale profitably while reinforcing its market leadership.

Competitive Landscape and Barriers to Entry

Figma operates in the dynamic and highly competitive market of collaborative design and prototyping software. While it has achieved significant market dominance, several key players offer similar functionalities or compete in adjacent spaces. The relatively small number of direct, large-scale competitors is a testament to the substantial barriers to entry in this market.

Competition

Figma’s primary focus is UI/UX design, real-time collaboration, and streamlining cross-functional product development workflows.

Canva:

Similarity: Canva is a cloud-based design platform that also employs a freemium model and targets a broad audience, including professionals and non-designers. It offers UI/UX design capabilities and robust collaboration features. Notably, 10% of Canva’s revenue now comes from enterprises, indicating its growing presence in the professional market that Figma serves.

Differences: Canva's strength lies in broader graphic design (e.g., social media graphics, presentations, marketing materials) and ease of use for everyday design tasks. While it has expanded into UI/UX, it is generally less specialized and powerful for intricate interface design or deep developer handoffs compared to Figma’s dedicated features like Dev Mode.

InVision:

Similarity: InVision was an early leader in cloud-based design and prototyping, focusing on collaboration and workflow integration for product teams. It offered features for prototyping, feedback, and design system management.

Differences: InVision has struggled to keep pace with Figma's rapid innovation and market share gains. Its collaboration features are generally considered less robust and seamless than Figma's real-time editing, and it lacks a direct equivalent to FigJam for whiteboarding. InVision has seen its market position erode significantly since Figma’s rise.

Framer:

Similarity: Framer is a web-based design tool primarily for UI/UX and interactive prototyping, with a strong emphasis on developer handoffs and creating code-based designs. It supports real-time collaboration and operates on a freemium model.

Differences: Framer typically appeals to a more niche audience of advanced designers and developers who prioritize interactive and code-friendly prototypes. Figma, while offering robust prototyping, serves a much broader audience, including those focused purely on static design, wireframing, and general graphic design.

Miro:

Similarity: Miro is a leading cloud-based visual collaboration platform focused on online whiteboarding. It directly competes with Figma’s FigJam product for brainstorming, ideation, and project management across cross-functional teams.

Differences: Miro is not a direct competitor in the core UI/UX design space. Its focus is entirely on visual collaboration and whiteboarding, making it a competitor to FigJam rather than Figma's core design tool. However, the overlap in team collaboration workflows makes it an important player in Figma's expanded addressable market.

Proto.io:

Similarity: Proto.io is another web-based prototyping tool for UI/UX design, offering collaboration features for teams.

Differences: Proto.io has a smaller market presence and is generally less feature-rich and scalable compared to Figma, particularly concerning enterprise adoption and comprehensive design system management.

Discontinued or Declining Competitors

Adobe XD: Adobe's direct competitor to Figma was officially discontinued in June 2023. Despite Adobe's vast resources, XD struggled to gain significant market share due to its reliance on integration with the costly Creative Cloud suite and its inability to match Figma's seamless real-time collaboration. It generated only $17 million in ARR in 2022, highlighting its competitive failure against Figma.

Sketch: Once a dominant force in UI/UX design, Sketch is a desktop-native tool limited to macOS. Its lack of inherent real-time collaboration and reliance on third-party plugins for cloud functionality has significantly hampered its ability to compete with Figma's browser-first approach. Its market share has been in steady decline.

In essence, there are approximately 5–6 active competitors with overlapping functionalities in cloud-based, collaborative design or prototyping (Canva, InVision, Framer, Miro, Proto.io, and other smaller niche players). However, none of these companies currently match Figma’s scale, market share (estimated 80% in product design by some surveys), or the comprehensive breadth of features across design, prototyping, whiteboarding, and developer handoffs within a single, unified platform. Moreover, its multiplayer canvas, powered by low-latency infrastructure and WebGL, is difficult to match. Beyond technology, Figma benefits from powerful cross-functional network effects and has become the industry standard by 2021, making it the default platform for many teams. Its community-driven ecosystem, extensive plugin library, and developer contributions further entrench user loyalty, while enterprise adoption by firms like Microsoft and Airbnb reflects the trust and scalability Figma has earned—capabilities that take years and capital to establish. Together, these elements create a durable moat that deters new entrants and limits the rise of comparable competitors.

Valuation

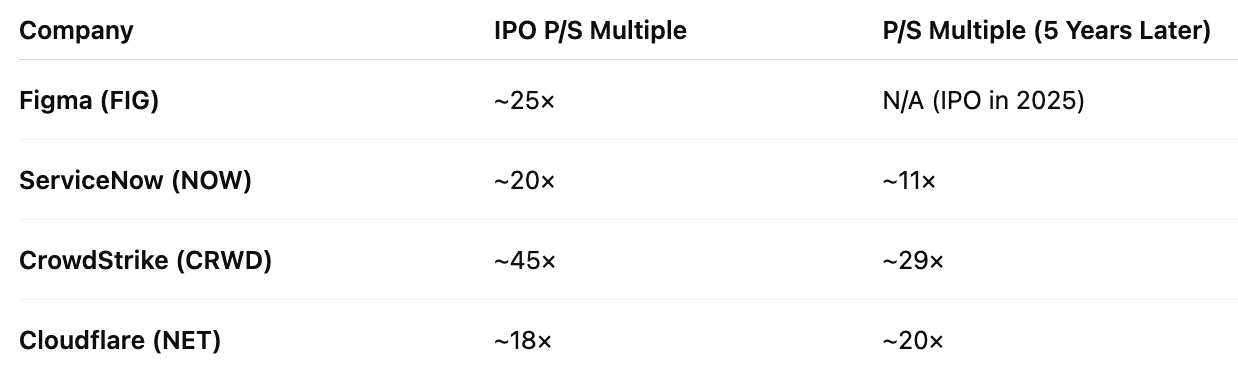

Figma is seeking an IPO valuation of approximately $19 billion. This valuation is higher than its $12.5 billion secondary market valuation in 2024 but lower than the $20 billion valuation associated with the failed Adobe acquisition in 2022. The proposed valuation implies a revenue multiple of approximately ~25 times its 2024 revenue of $749 million.

Forecasting Figma's future revenue by 2030 requires a nuanced approach, considering its current market dominance, growth drivers, competitive landscape, and the transformative potential of AI. We will present bear, base, and bull case scenarios, translating these into revenue projections based on available data and industry trends. All projections are inherently speculative and dependent on future market dynamics.

IPO Valuation

Figma's expects an IPO valuation of $19 billion, with a projected share price between $30 and $32. The estimated fully diluted share count is 607.5 million. This figure includes 487.5 million shares outstanding post-offering plus approximately 120 million shares from unvested equity awards such as RSUs, stock options, and warrants. We compare below Figma’s P/S multiple with other SaaS IPOs with similarly strong product portfolios. We think Figma will close IPO with higher than 25x P/S multiple.

Total Addressable Market (TAM)

Figma holds an estimated 80% market share in product design, firmly positioning itself as the leader in UI/UX design and prototyping. It’s also expanding into adjacent collaborative domains with products like FigJam and Figma Slides. The company estimates a $33 billion TAM, derived from an IDC-commissioned report forecasting 144 million global professionals engaged in software design by 2029. By applying internal pricing data to these IDC figures, Figma arrives at its TAM projection.

Figma expects to benefit from the rise in digital products and the democratization of software creation through generative AI—IDC forecasts over 1 billion new apps by 2028. As design becomes central to brand identity, Figma believes thoughtfully designed user experiences will distinguish winning products. It also anticipates innovation in AI-native interfaces and interaction models, further expanding its relevance.

Despite 78% of Forbes Global 2000 companies using Figma by March 2025, only 24% spent more than $100,000 in ARR, suggesting significant whitespace for growth within large enterprises. This internal expansion potential represents a major lever for TAM realization.

Valuation Scenarios

Projections are based on an annualized Q2 2025 revenue of ~$1 billion, applying different CAGRs to account for market, AI, and competitive dynamics.

Bear Case: Slowed Growth and Headwinds

Revenue CAGR: 15% → 2030 Revenue ≈ $2B

Valuation Multiple: 15× P/S → 2030 Valuation ≈ $30B

Share Count (2030): ~704M (assuming 3% CAGR from 607.5M)

Implied Per Share Price: ≈ $42.60

Outcome: ~6.6% CAGR in share price from IPO midpoint of $31

Bear Case Risks:

AI Disruption: Generative AI reduces need for human designers and collaboration seats

Rising Competition: Canva and Miro encroach on core and adjacent markets; AI-native startups accelerate disruption

Global Headwinds: Economic stagnation, rising tariffs, geopolitical risk hinder international growth (53% of current revenue)

Ineffective M&A: Acquisitions fail to create meaningful value

Base Case: Steady Growth and Execution

Revenue CAGR: 20% → 2030 Revenue ≈ $2.5B

Valuation Multiple: 20× P/S → 2030 Valuation ≈ $50B

Share Count (2030): ~775M (from 607.5M at 5% CAGR)

Implied Per Share Price: ≈ $64.49

Outcome: ~15.8% CAGR in share price from IPO midpoint of $31 — still compelling, though moderated by share dilution.

Base Case Drivers:

Product-Led Growth (PLG): Freemium model and 132% NDR sustain growth within existing accounts

Enterprise Expansion: $100K+ ARR customers grow 30% YoY

Balanced AI Integration: AI augments designers rather than replaces them

Global Expansion: International revenue increases to 60% via localization

Strategic M&A: Modest success from targeted acquisitions like Payload CMS

Constraints:

Competitive pressure from Canva/Miro caps further market share expansion

AI adoption evolves gradually, not enough to revolutionize seat count

Bull Case: Category Dominance and AI Tailwinds

Revenue CAGR: 25% → 2030 Revenue ≈ $3B

Valuation Multiple: 25× P/S → 2030 Valuation ≈ $75B

Share Count (2030): ~813M (from 607.5M at 6% CAGR)

Implied Per Share Price: ≈ $92.25

Outcome: ~24.4% CAGR in share price from IPO midpoint of $31 — exceptional return, driven by strong growth and premium multiple.

Bull Case Catalysts:

AI Leadership: Figma pioneers agentic AI tools, making AI a core differentiator and workflow enhancer

Aggressive, Successful M&A: $1.5B IPO cash deployed in high-impact deals (e.g., CMS, no-code, AI startups)

Global Market Dominance: Non-U.S. revenue climbs to 70%, with regional GTM strategies and offices in Singapore, Berlin, and Tokyo

Full Product Suite Adoption: Widespread use of FigJam and Slides across non-design roles boosts seat expansion

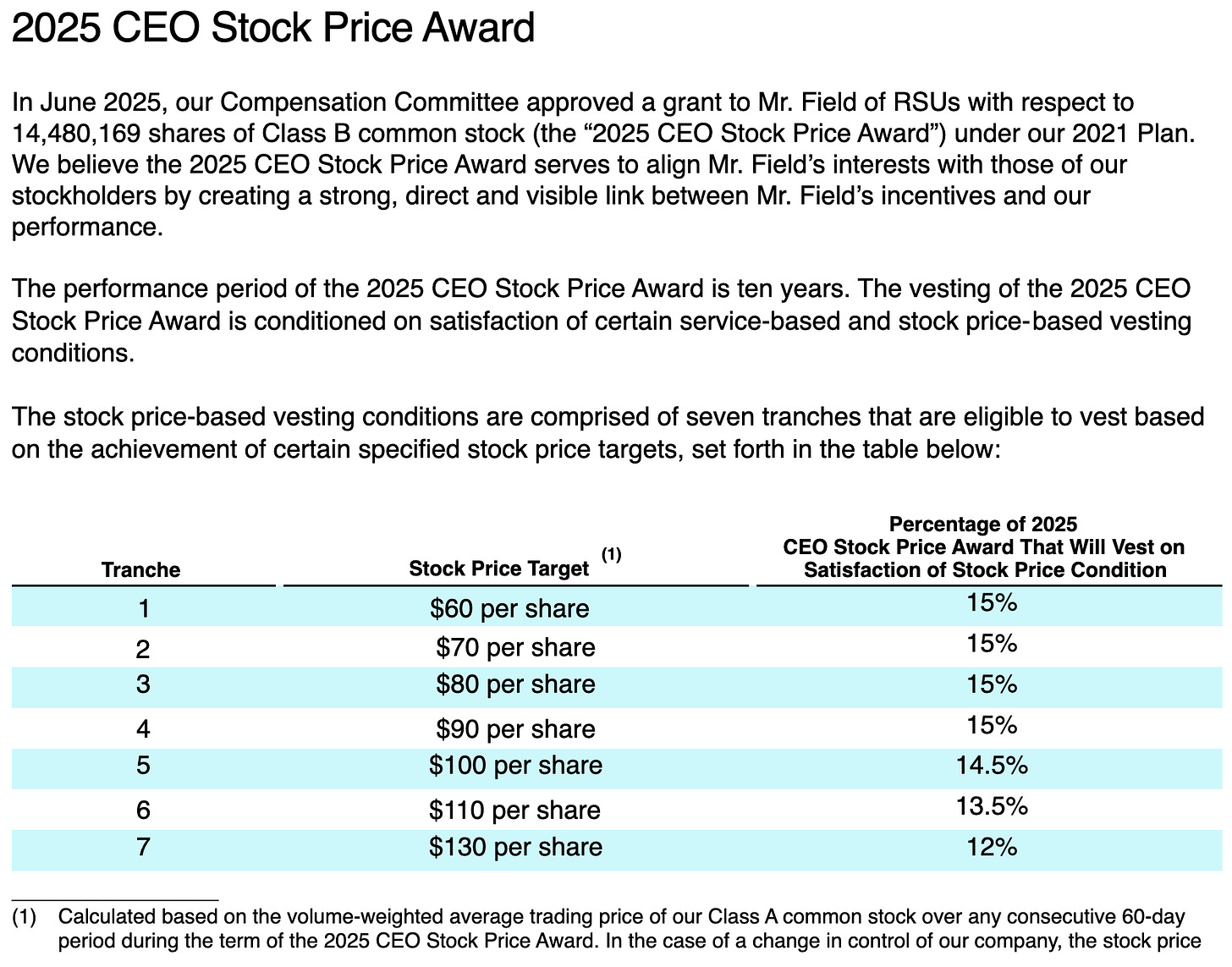

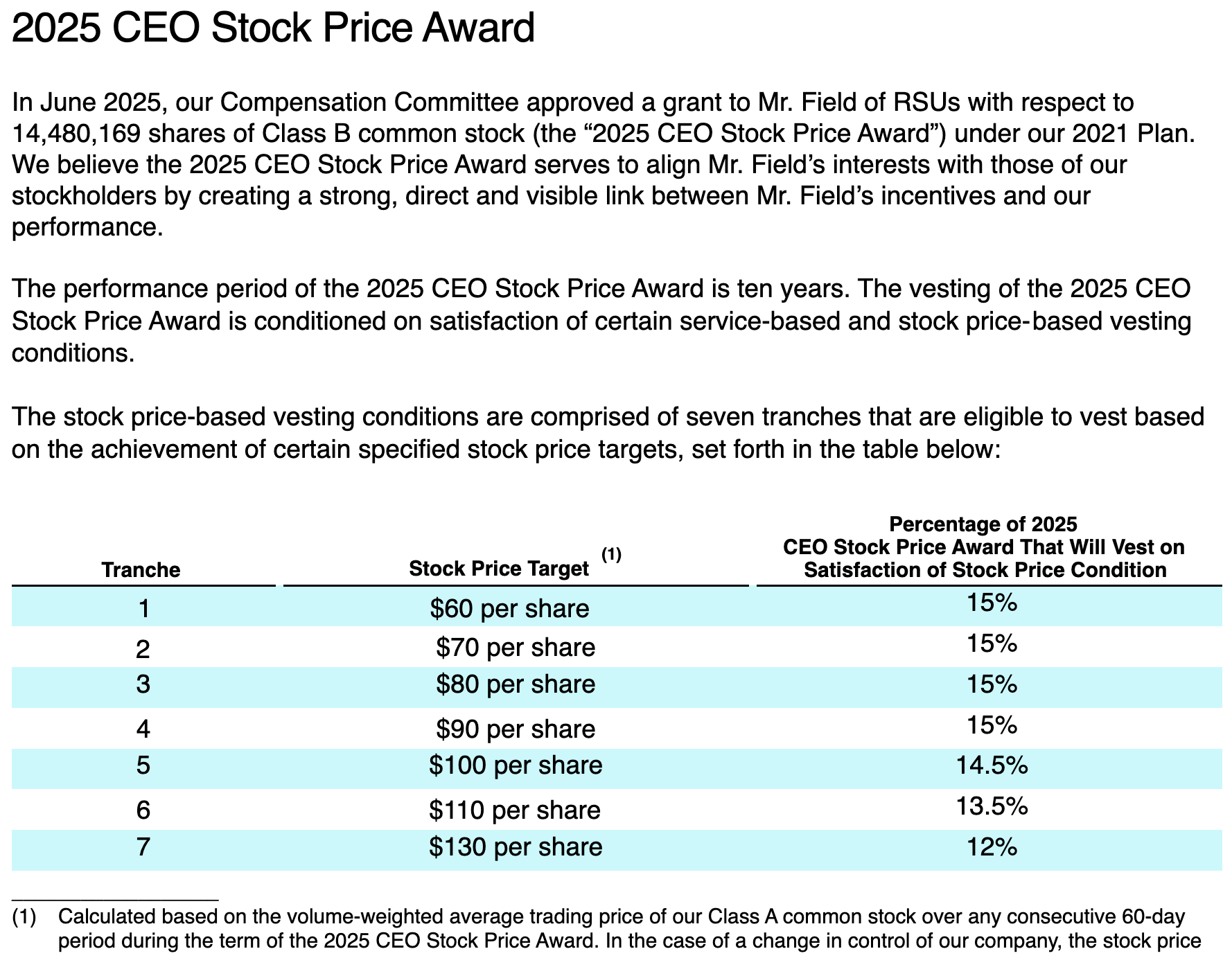

In June 2025, the board approved a long-term incentive package for the CEO tied directly to share price performance over the next ten years. The award includes 14.48 million RSUs that vest only if the stock reaches aggressive milestones, with no payout unless price targets are met.

Risks:

Execution must remain flawless amid high expectations

Premium valuation could result in volatility if Figma under-delivers

Final Thoughts

Figma represents a compelling investment for those with a strategic long-term view and an appetite for growth-oriented technology stocks. Its core business model is robust, leveraging ingenious counter-positioning against established giants like Adobe and Sketch through its pioneering cloud-based, real-time collaborative platform. The company's impressive financial performance, characterized by strong revenue growth, expanding enterprise client base, and improving profitability, underscores the efficacy of its product-led and community-led growth strategies.

Crucially, Figma operates with characteristics of a Scale-Economies-Shared (SES) model. By offering a powerful freemium tier, continuously enhancing features for existing subscription prices, and fostering a vibrant, user-contributed ecosystem, Figma effectively shares the benefits of its growing scale with its users. This strategy not only drives widespread adoption but also cultivates deep customer loyalty and creates powerful network effects, acting as a significant barrier to entry for potential competitors.

While the number of direct, large-scale competitors is relatively small, reflecting the formidable technological, market, and capital barriers to entry, Figma is not without its challenges. The rapid evolution of AI-driven design tools poses both a transformative opportunity and a potential risk, as it could reshape design workflows and impact future seat counts. Furthermore, intense competition from well-funded players like Canva and Miro in adjacent collaboration spaces, coupled with macroeconomic headwinds and international market volatility, demands ongoing vigilance.

For growth-oriented investors with high risk tolerance and a 5-year time horizon, Figma represents a strong business with undeniable category leadership in collaborative UI/UX design. Its product-led growth engine, 132% net dollar retention, 88%+ gross margin, and deep enterprise traction position it well to benefit from secular trends like AI-driven productivity and the global proliferation of digital tools. However, while the fundamentals are promising, the valuation leaves limited room for upside. At the IPO midpoint of $31 per share (valuing the company at ~$19 billion fully diluted), our base case, with aggressive assumptions around AI execution and global expansion, projects a ~16% CAGR. In short, Figma may be a great company, but at IPO valuation, it’s not obviously a great stock.

I only plan to initiate a position in Figma at 0.5% of my overall portfolio allocation, if the price goes below $30 per share. At this level, I believe the base case offers a compelling risk-reward profile, even accounting for execution risks related to competitive dynamics and the pace of enterprise adoption. My conviction is further supported by firsthand experience using the product—its intuitive interface, real-time collaboration, and cross-functional utility are best-in-class. I see Figma as uniquely positioned to capitalize on the secular trend of software proliferation, especially with IDC projecting over 1 billion new applications to be built in the coming years. As businesses increasingly prioritize design quality and user experience, I believe Figma will remain a foundational tool in the product development stack.

© 2025 InsightButter LLC. All rights reserved.

All content published on PennyInsight, including articles, newsletters, comments, and any other materials (collectively, "Content"), is provided for educational purposes only and for general informational use.

The Content is not, and should not be construed as, investment advice, financial advice, or a recommendation to buy, sell, or hold any security or other financial instrument. We do not provide personalized financial planning or investment services. Always consult with a qualified financial professional before making any investment decisions. Reliance on any information provided by PennyInsight is solely at your own risk.